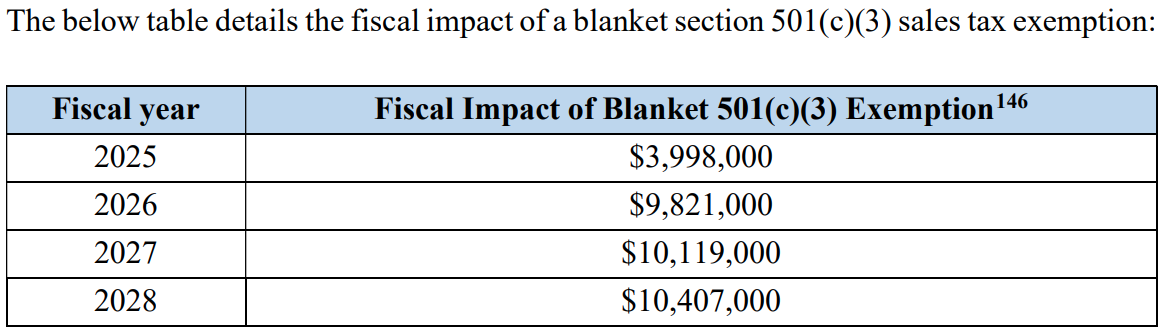

Gov. Janet Mills has proposed extending a sales tax exemption to all nonprofits operating in Maine, which state officials say will address inequities among organizations seeking exemption and simplify the tax exemption process, but will cost the state about $10 million annually.

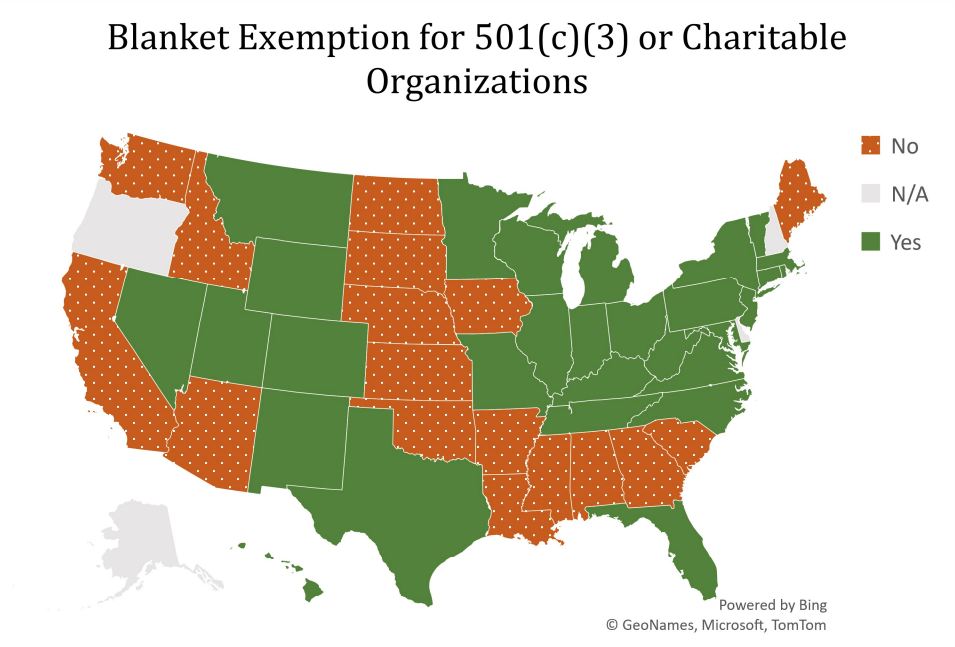

Of the 47 states with sales tax, Maine is among only 17 — and the only one in New England — without a blanket exemption for nonprofits, according to a report released last month by Maine Revenue Services.

Mills said in a statement that extending the exemption to all nonprofits “eliminates the need for the legislature to pass a new statutory exemption for every nonprofit seeking tax-exempt status and is consistent with the treatment of nonprofits in most other sales tax states.”

The proposal, which is included in the governor’s supplemental budget, would make any nonprofit that is exempt from federal income tax under the Internal Revenue Service automatically exempt from state sales tax on items purchased as part of an organization’s mission.

The move would make more than 5,200 organizations newly eligible for sales tax exemption, according to the report.

Hospitals and churches have been exempt from the tax since it went into effect in 1951. The legislature has added several dozen categories to the list over the years, including volunteer fire departments, veterans’ service organizations, and nonprofit child care centers, nursing homes and historical societies.

Maine Revenue Services still receives between 100 and 200 applications each year from nonprofits that think they qualify. Most are eventually approved, but “gray areas” in the law result in a “fair amount of confusion for organizations,” according to the report, and require staff to spend “time and resources on education, customer assistance, and administration to ensure that the law is carried out as intended.”

Mary Alice Scott, public affairs manager of the Maine Association of Nonprofits, called the current law regarding sales tax exemptions “unusual, unfair, confusing and inefficient.”

“It makes sense for every 501(c)(3) organization to receive the same treatment when it comes to sales tax,” Scott told The Maine Monitor. “The IRS recognizes that they are all doing work for the public good; Maine should recognize that, too.”

Lawmakers in 2020 tried to pass a blanket nonprofit exemption as part of a bill that included other measures related to service provider tax and income tax, but the bill died in the House.

The blanket nonprofit exemption was proposed again last session, but was later amended to instead instruct Maine Revenue Services to study the impact of the measure.

Scott said the confusing nature of the existing system is likely why previous attempts to pass a blanket sales tax exemption have been unsuccessful: “Many organizations review the current list of exemptions and come away having no idea if they are included or not, so you can imagine it was confusing for lawmakers, too.”

A number of nonprofits testified in support of the blanket exemption last year. Many said the few hundred dollars spent on sales tax could make a significant difference if redirected to those they serve.

The Maine Coalition Against Sexual Assault said sexual assault survivors can spend hours in the hospital when they go through forensic examination, and that when sexual assault centers accompany them, they put together bags of essential supplies such as sweatsuits, nail files, snacks and water. When the centers buy these items, they pay sales tax.

The coalition also manages emergency funds it gets from the federal government through the Victim of Crime Act for the work it does with survivors, Melissa Martin, public policy and legal director, told the Monitor.

The coalition uses those funds to buy essentials for people experiencing sex trafficking who don’t have stable housing. In one example of a $70,000 purchase for those uses, the coalition paid nearly $4,000 in tax.

Martin said a blanket exemption would allow nonprofits to spend more money on their service work and less time on administrative tasks related to applying for an exemption.

“Are nonprofits going to spend time getting that exemption or are they going to spend time doing their direct service work? I think most organizations have made the choice to spend the time doing their important direct service work,” she said.

Lisa Thomas-Willey, assistant to the executive director at Ruth’s Reusable Resources, which redistributes unwanted office supplies from businesses and gives them to teachers for their classrooms, said the current sales tax exemption system unfairly excludes some nonprofits, is inefficient for retailers and lawmakers, and “it is arbitrary and unclear why some nonprofits are included while others are not.”

Ruth’s Reusable Resources receives $10,000 to $15,000 annually for its Tools for School backpack program, but $550 to $780 of that grant goes to sales tax, Thomas-Willey said.

“We could provide 50-70 additional backpacks each year with the money we pay in sales tax for the school supplies.”

Trekkers, a youth mentoring nonprofit in Rockland that helps young people from rural Maine navigate adulthood, said it paid nearly $6,000 in sales tax in 2022, which was equivalent to 2 1/2 months of its meal budget to feed the students.

There are more than 7,000 501(c)(3) nonprofit organizations in Maine as of 2018, according to the Maine Association of Nonprofits. Most have annual expenditures of less than $100,000. Nonprofits employ more than 100,000 Maine workers.

Maine sales tax law currently has 56 provisions exempting different types of organizations, most requiring the applicant to be a nonprofit, according to the state report.

“While these exemptions are valuable to the organizations that qualify, Maine’s current patchwork of narrowly crafted exemptions creates inequities between similar organizations and confusion for taxpayers, leaving some nearly identical organizations with different eligibility,” according to the Maine Revenue Service.

In a Feb. 15 presentation to the legislature’s Taxation Committee, Peter Lacy, an attorney with office of tax policy for the Department of Administrative and Financial Services, said that just since 2015 the legislature has approved exemptions for numerous groups, including veteran service organizations, heating assistance organizations, youth camps, nonprofit pet food assistance organizations, cemetery companies and areas agencies on aging.

In response to concerns the sales tax exemption could result in an additional loss of property tax to local communities, Lacy told committee members the measure would not impact a nonprofit’s status for property tax exemptions.

Rep. Joe Perry, D-Bangor, said that during his time on the committee, he’s reviewed numerous bills asking for nonprofit expansions and has never seen one come back and ask for additional property tax exemptions.

“I would have zero concern from my experience on the committee that this is a slippery slope,” he said.

The MRS report argues a clear standard will benefit taxpayers, lawmakers and the state by clearing up confusion and reducing the time spent on processing applications or considering exemptions.

“To the extent possible, tax law should be simple and accessible to the public,” MRS wrote in the January report. “Similarly situated organizations should receive similar tax benefits, and a blanket exemption for 501(c)(3) organizations would be a significant step towards the goal of creating a fairer, simpler sales tax.”

The proposed exemption will next go before the Appropriations and Financial Affairs Committee as part of the supplemental budget.